Now, onto what we do and don’t know about these tax incentives.

WHAT’S NEW ON LOW-INCOME TAX CREDITS IN THE GUIDANCE

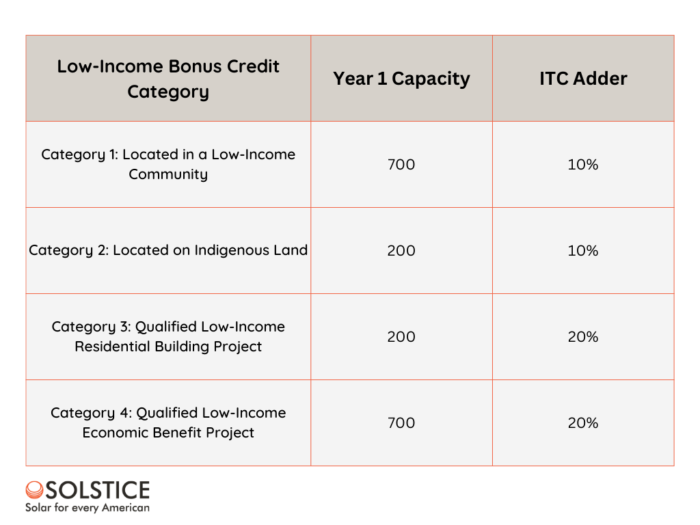

- Allocation: Breakdown (below) of the first 1.8 GW across four low-income bonus credit categories

- Application: Applications across categories will open in phases, offering 60-day windows

- Timeline: The order of categories: 3 and 4 in Q3 2023; then 1 and 2 to follow

- Admin: DOE will review applications and lead allocation processes

- Eligibility: Projects that energize before being awarded an allocation will not receive the credit

NEXT ROUND OF GUIDANCE: WHAT TO LOOK FOR

The first round of guidance mentions forthcoming guidance and additional criteria 10 times throughout the 10-page document. What exactly does a project need to have/commit to for qualification in each category? How and what should be prepared ahead of the application windows? For now, we’re still waiting for the answers that developers and asset owners need to update project plans and models.

All Categories

- How applications will be scored and awarded

- What will be required for eligible applications

Categories 1 & 2

- Site control

- Interconnection agreements

- Completed utilities studies

- State and local permits

- Letters of support (category 2)

Categories 3 & 4

- How to define and assess the financial benefits that must be provided

- Acceptable income verification methods

- Potentially ranging from self-attestation and geo-eligibility to proof of income or participation in income-based assistance programs

- Required plans to distribute benefits equitably

- Required list of eligible beneficiaries and capacity allocation

- Reporting requirements

- Required building verification (category 3)

- Required statements from residents agreeing to distribution of benefits (category 3)

The only new information relevant to improving your application is that the following items may boost your chances of being awarded capacity:

- Ownership or development by community-based organizations and mission-driven entities

- Intent to include new market participants

- Above-and-beyond bill savings for low-income communities and marginalized individuals

- High degree of commercial readiness

The timeline for forthcoming guidance is up in the air but leading trade groups and industry stakeholders have already requested meetings with Treasury and are pushing for more guidance ASAP. Solstice will continue to stay engaged on advocacy to the White House, Treasury Department, IRS, and DOE.

INDUSTRY REACTION

Beyond the overall feeling that this round of guidance largely kicks the can down the road and was only issued this early in order to comply with the IRA’s legislative requirements, there are a couple other pieces of commentary worth mentioning.

As explained above, the four categories of capacity are broken down by bonus credit type, instead of project sector (e.g. community solar / residential projects / multi-family residential / etc.), which would likely make application reviews more efficient and consistent. The proposed breakdown will pit projects with significantly different structures — both in development cycles and delivery of benefits — against each other for capacity. As of now, community solar projects could fit into any of these categories, but we’ll be on the lookout for upcoming eligibility criteria that could change that.

The guidance suggests that a lottery may be used when there’s an excess of eligible applicants by category, but it leaves room for DOE to decide on other processes instead.

Interested in working with Solstice? Schedule a call to meet with our business development team at bd@solstice.us.